Get In Touch

Undoubtedly, 2025 has been a year full of surprises for Indian investors. From midcap volatility to sharp rallies in PSUs, global uncertainty, to stable domestic flows - the market taught us many lessons.

And, now that a few weeks are left for 2026 to begin, here's what happened in markets and what lessons investors should take in return.

In this guide, we will cover the top market lessons 2025 has taught us and what market outlook PMS has for the next year.

2025 clearly showed that midcaps and small caps can create strong wealth, but they also come with big swings. Both segments saw strong rallies during the year, followed by sudden corrections. Overall returns stayed positive, but the path was very uneven.

Many investors chase these segments for higher returns. And it's true - when midcaps and small caps turn bullish, portfolios pick up quickly. And that's because a few stocks might be driving the entire portfolio, not all might be yielding positive returns.

But the same speed applies on the downside, which is where most people get caught off guard.

What 2025 taught us:

In short, midcaps and small caps rewarded investors in 2025 - but only those who stayed prepared for the volatility that comes with them.

For PSUs (Public Sector Undertakings), 2025 was a turning point. With the Union Budget placing greater emphasis on this space, government-led projects gained momentum, capex cycles strengthened, balance sheets improved, and dividend payouts rose. The overall sentiment around PSUs shifted meaningfully.

A clear example of this shift was SBI's strong performance, delivering about 25% gains in 2025 (as of December 1). This rally, along with broader strength in PSU banks and industrial PSUs, pushed many portfolios to increase their PSU allocations.

In FY2025, multiple peers outperformed, with notable returns like Hindustan Copper (68.4%), NALCO (55.6%), Chennai Petroleum (50.9%), BEL (35.1%), BHEL (28.3%), and IOC (28.2%).

During this time, PSUs' share in the Indian equity market (by market-cap) rose from roughly 10.1% in FY22 to ~15.3% by mid-2025. Even fundamentally, the PAT CAGR compounded by 36% between FY 2020 and FY 2025.

Often, PSUs are seen as "cheap stocks that never move." But when fundamentals improve (whether through higher earnings, cleaner debt levels, or better capital allocation), the market does support them.

There's one structural shift 2025 made this absolutely clear: Indian markets are no longer FII-dependent.

Throughout the year, domestic investors (retail, SIPs, DIIs, and HNIs) kept the market anchored even when global sentiment turned risk-off.

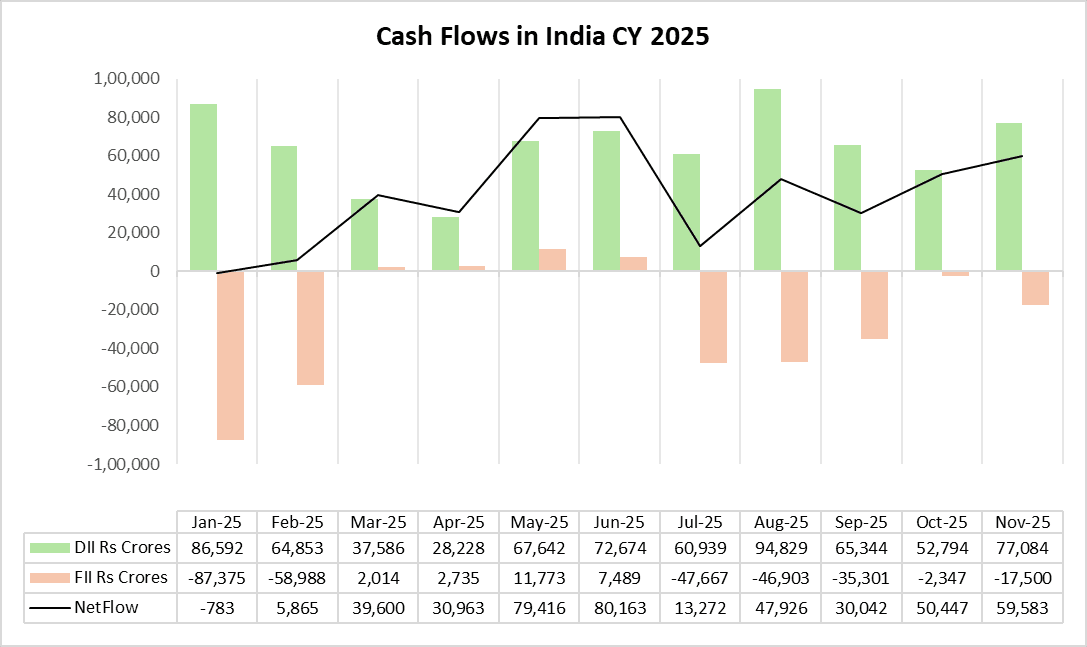

This chart itself tells the story.

Source: Moneycontrol

From January to November 2025, FIIs saw multiple months of heavy outflows — January, February, July, August, and September being the most prominent. These were periods when global markets were dealing with:

Each of these triggered short-term FII selling in emerging markets, India included.

But despite these outflows, the Nifty stayed resilient, and the reason is clear — DIIs kept buying consistently.

Across almost every month, the green bars on the chart (DII net inflows) are strongly positive, often ₹40,000 crore to ₹90,000 crore. This buying absorbed the FII exits.

Over here, clearly, the period between March and June 2025, the FIIs did invest in India (yellow bars), considering the following factors: India's macro stability: low inflation + strong GDP prints.

The takeaway is simple – “Even when FIIs sold, the market held steady because domestic investors continued buying with conviction.”

Across the multiple corrections we saw in 2025, one pattern remained consistent: Quality companies declined less, stabilised sooner, and recovered faster.

These are businesses with:

Whenever the market turned volatile (especially during FII sell-offs), these companies acted as "shock absorbers" in portfolios. Hence, the choice of having quality investments or stocks that are often tagged expensive comes with equal protection.

2025 made one thing very clear – stories don't move stocks for long, earnings do. A few "hyped" sectors like IT, FMCG, and Pharma couldn't keep up because their quarterly numbers didn't justify the optimism. Growth slowed, margins tightened, and guidance remained weak, so even good narratives couldn't save the stock prices.

Meanwhile, the so-called boring sectors, like utilities, railways, defence, power, and PSUs, quietly kept delivering solid earnings. For the short term, the stories (trends) can move stock prices for a few months. But, eventually, the earnings move stock prices for years.

Among all the lessons of 2025, this one stands out the most. Despite global noise, political headlines, tariff-cut announcements, and bouts of volatility, Indian investors showed a clear behavioural shift.

Earlier, any major global event would instantly drag Indian markets down. But in 2025, the narrative changed.

While the world was dealing with:

And the reason is simple:

Investors, too, evolved. They reacted less to global panic and focused more on fundamentals at home.

2025 proved that India has moved from being a market influenced by global sentiment to a market driven by domestic conviction.

In 2025, leadership rotated among manufacturing, capital goods, PSU, financials, pharma, and consumption – no sector remained a winner forever. Every year, India's market cycles shift, and what worked brilliantly last year may deliver muted returns the next.

At such times, when any sector can lead the market game, having a dynamic and research-driven allocation is essential. If you insist on a static portfolio, it may underperform when these cycles shift.

No doubt, the second half of 2025 was the year of silver and gold. With gold hitting all-time highs and debt yields becoming attractive, 2025 showed the value of multi-asset investing.

When markets turn unpredictable, having a mix of equity, gold, ETFs, and debt acts like a safety net. Each asset class reacts differently to global events, so when one dips, another often holds up or even outperforms. That balance is what protects a portfolio in volatile phases.

We saw several instances this year where the headline indices were rallying… yet most stocks weren't.

A clear example was when Reliance, HDFC Bank, and SBI saw sharp moves. Nifty jumped, the news looked bullish, but underneath, more than half of Nifty 500 stocks were either flat or negative during the same period.

So when the index shoots up, it doesn't always reflect broad-market strength.Often, it just means a few heavyweights are pulling the entire index upward.

The index may look green, but that's usually because just a few big companies are moving, not the whole market./p>

So if your portfolio holds stocks that aren't part of those few winners, it's natural for your returns to feel different from the index. Your portfolio isn't wrong – a handful of heavyweights is just carrying the index.

If 2025 taught investors anything, it's that emotions are expensive. Every year, investors fall into this trap, and it has to be the top market lesson for this year.

Markets dipped, rallied, corrected, and surprised, unlike any cycle. But those who stayed calm did far better than those who panicked or chased every rally. It's like following everyone's advice and ending up with the wrong choices.

At the end of the day, the golden rule still holds: "Control your emotions, and the markets will hurt you a lot less."

To sum up, 2025 was a year marked by PSU stocks, FIIs outflows, global uncertainty, the US Tariff war, sectoral growth, a commodity boom (such as gold and silver), and much more. However, in this market, predicting the next big trend can be tough.

While volatility never leaves, having a portfolio fund manager or opting for PMS (Portfolio Management Services)can be a savior. With their market experience and risk management tactics, investors can safeguard their investment and find avenues for growth.